ONE SIZE DOES NOT FIT ALL

Higher initial withdrawal rates or overly conservative portfolios can put your retirement at risk. But setting it too low can lead to sacrifices in retirement. You may want to consider a dynamic approach to spending.

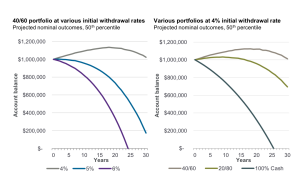

Setting an initial withdrawal rate and an appropriate portfolio allocation is necessary to sustain 30+ years of spending in retirement. The chart on the left illustrates the effects of different initial withdrawal rates assuming a 40% equity / 60% bond allocation. The 4% initial withdrawal rate—a general rule of thumb introduced in 1994, which adjusts the initial withdrawal amount for inflation over time to preserve purchasing power—is valid as is 5% but the 6% initial withdrawal rate proves not as successful and may put retirement at risk. The right chart illustrates the 4% withdrawal rate, but assuming various portfolio allocations. The more conservative the investor, the more difficult it may be to sustain the 4% rule over long periods of time. Consider a more dynamic approach to ensure that you efficiently use your savings to support your lifestyle while ensuring that you don’t run out of assets too quickly.