Six Simple Truths About Volatility

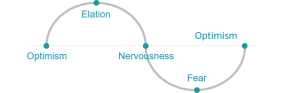

Volatility is back. Just as many people were starting to think markets only ever move in one direction, the pendulum has swung the other way. Anxiety is a completely natural response to these events. Acting on those emotions, though, can end up doing us more harm than good.

Volatility is back. Just as many people were starting to think markets only ever move in one direction, the pendulum has swung the other way. Anxiety is a completely natural response to these events. Acting on those emotions, though, can end up doing us more harm than good.

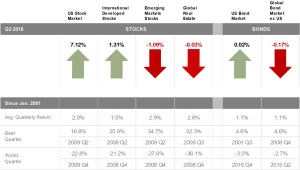

There are a number of tidy-sounding theories about why markets have become more volatile. Among the issues frequently splashed across newspaper front pages: global growth fears, rising interest rates, policy uncertainty, geopolitical risk, and trade issues.

In some ways, the increase in volatility in recent weeks could be just as much a reflection of the fact that volatility has been very low for some time.

So, the increase in market volatility is an expression of uncertainty. Markets do not move in one direction. If they did, there would be no return from investing in stocks and bonds. And if volatility remained low forever, there would probably be more reason to worry.

As to what happens next, no one knows for sure. That is the nature of risk. In the meantime, investors can help manage their risk by diversifying broadly across and within asset classes.

For those still anxious, here are six simple truths to help you live with volatility:

1. Don’t make presumptions

Remember that markets are unpredictable and do not always react the way the experts predict they will.

2. Someone is buying

Quitting the equity market when prices are falling is like running away from a sale. While prices have been discounted to reflect higher risk, that’s another way of saying expected returns are higher. And while the media headlines proclaim that “investors are dumping stocks,” remember someone is buying them. Those people are often the long-term investors.

3. Market timing is hard

Recoveries can come just as quickly and just as violently as the prior correction. For instance, in March 2009—when market sentiment was at its worst—the S&P 500 turned and put in seven consecutive months of gains totaling almost 80%. This is not to predict that a similarly vertically shaped recovery is in the cards, but it is a reminder of the dangers for long-term investors of turning paper losses into real ones and paying for the risk without waiting around for the recovery.

4. Markets and economies are different things

The world economy is forever changing, and new forces are replacing old ones. This applies both between and within economies. For instance, falling oil prices can be bad for the energy sector but good for consumers. New economic forces are emerging, as global measures of poverty, education, and health improve.

5. Nothing lasts forever

Just as smart investors temper their enthusiasm in booms, they keep a reserve of optimism during busts. And just as loading up on risk when prices are high can leave you exposed to a correction, dumping risk altogether when prices are low means you can miss the turn when it comes. As always in life, moderation is a good policy.

6. Discipline is rewarded

The market volatility is worrisome, no doubt. The feelings being generated are completely understandable and familiar to those who have seen this before. But through discipline, diversification, and understanding how markets work, the ride can be made bearable. At some point, value re-emerges, risk appetites reawaken, and for those who acknowledged their emotions without acting on them, relief replaces anxiety.

If you’d like to discuss your specific investment situation, please do not hesitate to call our office.

All expressions of opinion are subject to change without notice. This article is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products or services. Diversification does not eliminate the risk of market loss. There is no guarantee investment strategies will be successful. The S&P 500 Index is not available for direct investment and does not reflect the expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results. Contributions from Dimensional Fund Advisors LP.