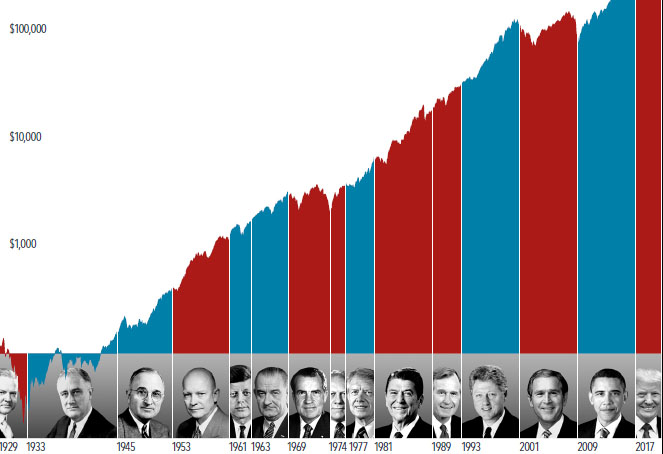

What History Tells Us About US Presidential Elections and the Market

It’s natural for investors to seek a connection between who wins the White House and which way stocks will go. But a look at history underscores that shareholders are investing in companies, not a political party.