Solo 401ks are cost-effective, powerful retirement vehicles. They are designed for self-employed workers who have no employees other than a spouse. They allow small-business owners to stash away much more for retirement than they could stash in a traditional IRA or a SEP IRA, while avoiding the expense and paperwork of setting up a full traditional 401(k) plan.

1) Generous Contribution Limits

For the plan year 2019, a participant under the age of 50 can make a maximum employee deferral in the amount of $19,000. This is also called an “employee” contribution. Age 50+ can contribute up to $25,000.

2) Ability to Self-Direct

With a Solo 401k, you can act as your own trustee. This eliminates the need for a bank or trust company to serve as a trustee. The plan participant (you) is in control of the plan.

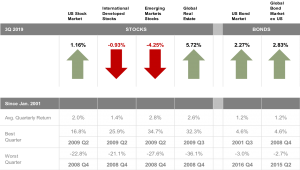

We have established many Solo 401k’s for individuals in our firm. Charles Schwab’s user friendly platform makes it easy to save aggressively.

3) Profit Sharing Provision

On top of the allowed employee deferral, the participant can also contribute up to 25 percent of total compensation to a profit-sharing component of the plan. This is often called an “employer” contribution.

Total combined plan contributions (employer and employee) cannot exceed the lower of $57,000 or 100 percent of compensation (plus any catch-up contributions if over the age of 50).

4) Contributions are Elective

Contributions to a solo 401k plan are entirely discretionary. A participant has the option of contributing to the plan and can reduce or even suspend plan contributions as necessary.

5) Ability to Take Out a Loan

A solo 401k allows participants to borrow up to $50,000 or 50% of their vested account value (whichever is lower). This loan can be made for any purpose with a payback period of up to 5 years.

This offers significant flexibility and provides flexibility against having to take a withdrawal that would be subject to a tax penalty. This flexibility is in contrast to an IRA that offers no participant loan feature.

6) Minimal Tax Filing Requirements

There are no annual filing requirements unless the solo 401k plan exceeds $250,000 in assets. The Solo 401k is extremely easy to administer.

7) Roth Contributions

Solo 401ks can include a Roth component. Just like Roth IRA contributions, Roth 401k contributions are made on an after-tax basis. Unlike a pre-tax contribution, there is no upfront tax deduction. However, a distribution of Roth 401k contributions (along with earnings) is tax-free.

Individual taxpayers are disallowed from contributing to a Roth IRA based on income restrictions. These same restrictions do not apply to Roth 401k contributions. A Roth 401k contribution has the same limitation as an employee deferral of $19,000. This is substantially more than the limit of a Roth IRA.

8) Rollover Provision

One key advantage is rollover flexibility. A solo 401k can accept rollovers from other retirement accounts, such as an IRA, a SEP, or a 401k from a prior employer. However, Roth IRAs cannot be rolled into a solo 401k.

SIGN UP FOR A FREE CONSULTATION BEFORE DECEMBER 31ST!