Investment fads come and go. Letting short-term trends influence your approach may be counterproductive to pursuing your financial goals.

Investment fads are nothing new. When selecting strategies for their portfolios, investors are often tempted to seek out the latest and greatest investment opportunities. Over the years, these approaches have sought to capitalize on developments such as the perceived relative strength of particular geographic regions, technological changes in the economy, or the popularity of different natural resources. But long-term investors should be aware that letting short-term trends influence their investment approach may be counterproductive.

“There’s one robust new idea in finance that has

investment implications maybe every 10 or 15 years,

but there’s a marketing idea every week.” Nobel laureate Eugene Fama

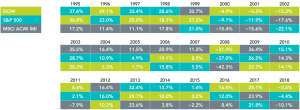

What’s Hot Becomes What’s Not

Let’s look back at some investment fads over the decades:

1950’s – the “Nifty Fifty” (50 hot companies) were all the rage.

1960s – “go-go” stocks and funds piqued investor interest.

Late 20th century – emergence of a “new economy”

1990s – attention turned to the rising “Asian Tigers” of Hong Kong, Singapore, South Korea, and Taiwan.

2000’s – “BRIC” countries of Brazil, Russia, India, and China and their new place in global markets.

In the wake of the 2008 financial crisis – “Black Swan” funds, “tail-risk-hedging” strategies, and “liquid alternatives” abounded.

Recently – peer-to-peer lending, cryptocurrencies, and even cannabis cultivation

The Fund Graveyard

Unsurprisingly, however, numerous funds across the investment landscape were launched over the years only to subsequently close and fade from investor memory. While economic, demographic, technological, and environmental trends shape the world we live in, public markets aggregate a vast amount of dispersed information and drive it into security prices. Any individual trying to outguess the market by constantly trading in and out of what’s hot is competing against the extraordinary collective wisdom of millions of buyers and sellers around the world.

With the benefit of hindsight, it is easy to point out the fortune one could have amassed by making the right call on a specific industry, region, or individual security over a specific period. While these anecdotes can be entertaining, there is a wealth of compelling evidence that highlights the futility of attempting to identify mispricing in advance and profit from it.

It is important to remember that many investing fads, and indeed, most mutual funds, do not stand the test of time. A large proportion of funds fail to survive over the longer term. Of the 1,622 fixed income mutual funds in existence at the beginning of 2004, only 55% still existed at the end of 2018. Similarly, among equity mutual funds, only 51% of the 2,786 funds available to US-based investors at the beginning of 2004 endured.

What Am I Really Getting?

When confronted with choices about whether to add additional types of assets or strategies to a portfolio, it may be helpful to ask the following questions:

1. What is this strategy claiming to provide that is not already in my portfolio?

2. If it is not in my portfolio, can I reasonably expect that including it or focusing on it will increase expected returns, reduce expected volatility, or help me achieve my investment goal?

3. Am I comfortable with the range of potential outcomes?

If investors are left with doubts after asking any of these questions, it may be wise to use caution before proceeding. In addition, there is no shortage of things investors can do to help contribute to a better investment experience. Working closely with a financial advisor can help individual investors create a plan that fits their needs and risk tolerance. Pursuing a globally diversified approach; managing expenses, turnover, and taxes; and staying disciplined through market volatility can help improve investors’ chances of achieving their long-term financial goals.

Conclusion

Fashionable investment approaches will come and go, but investors should remember that a long-term, disciplined investment approach based on robust research and implementation may be the most reliable path to success in the global capital markets.

{kind=link}

{kind=link}

{kind=link}