Video series: Retirement Readiness #2 – How Much Should I Save for Retirement?

Check out this second installment of the Retirement Readiness series! How much should you save for retirement? Marlena Lee, PhD, discusses important factors that can help you meet your goals, like determining your savings rate, monitoring your progress, and making adjustments over time. This My Retirement Income Calculator can help give you a sense of how much income your savings could provide in retirement.

Video series: Retirement Readiness #1 – Monitoring Your Progress

When planning for retirement, it’s important to keep in mind how much spending your savings can support. The decisions you make today can help improve your retirement readiness. Beyond determining how much money to save, it’s useful to think about retirement in terms of how much income you’ll need after you stop working. Dimensional’s My Retirement Income Calculator can help give you a sense of how much income your savings could provide in retirement. Enjoy our Retirement Readiness series [...]

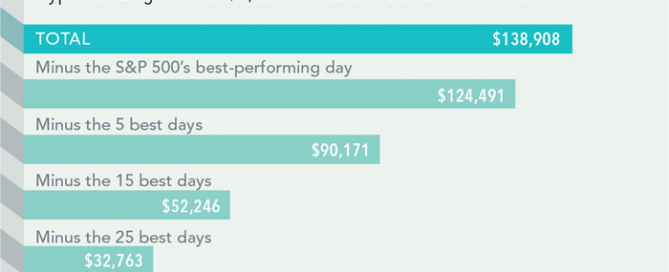

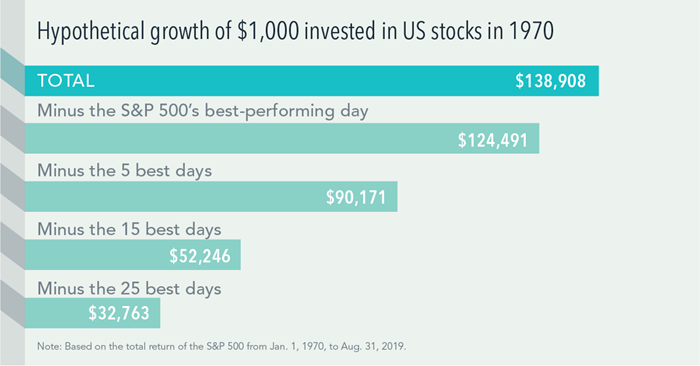

What Happens When you Fail at Market Timing?

It’s hard to predict the best days in the markets, and the cost of missing them can be high. The impact of missing just a few of the market’s best days can be profound, as this look at a hypothetical investment in the stocks that make up the S&P 500 Index shows. A hypothetical $1,000 turns into $138,908 from 1970 through the end of August 2019. Miss the S&P 500’s five best days and [...]

October Performance Dashboard

U.S. equities posted gains in October, bolstered by optimism around trade talks with China, strong earnings, and easing from the Fed, although Chairman Powell signaled a likely pause on future rate cuts. The S&P 500® and the S&P SmallCap 600® both gained 2%, while the S&P MidCap 400® gained 1%. International markets also gained, with the S&P Developed Ex-U.S. and the S&P Emerging BMI both up 4%. Enhanced Value continued to outperform in October, and Value again outperformed [...]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Kids’ future or yours? 6 Tips to Balance College and Retirement

Get the facts about saving for retirement and college at the same time. Understanding that funding each is equally important, and that even a late start is a good start. Every dollar saved is a dollar you don't have to borrow.