April Performance Dashboard

U.S. equities gained steam in April, powered by positive earnings, potential progress in U.S./China trade talks, and recent dovish sentiment from the Fed. The S&P 500®, the S&P MidCap 400® and S&P SmallCap 600® all gained 4%, and the VIX® declined to 13.12.

All U.S. equity factors rose in April, with High Beta and Enhanced Value taking the lead. Across sectors, Financials and Communication Services were the top performers, up 9% and 7%, respectively, while Health Care was the laggard.

The Index Bogeyman

Over the last several years, index funds have received increased attention from investors and the financial media.

Some have even made claims that the increased usage of index funds may be distorting market prices. For many, this argument hinges on the premise that indexing reduces the efficacy of price discovery. If index funds are becoming increasingly popular and investors are “blindly” buying an index’s underlying holdings, sufficient price discovery may not be happening in the market. But should the rise of index funds be a cause of concern for investors? Using data and reasoning, we can examine this assertion and help investors understand that markets continue to work, and investors can still rely on market prices despite the increased prevalence of indexing.

Many buyers and sellers

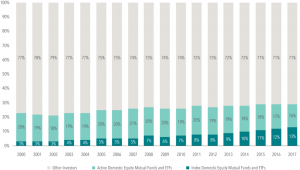

While the popularity of indexing has been increasing over time, index fund investors still make up a relatively small percentage of overall investors. For example, data from the Investment Company Institute shows that as of December 2017, 35% of total net assets in US mutual funds and ETFs were held by index funds, compared to 15% in December of 2007. Nevertheless, the majority of total fund assets (65%) were still managed by active mutual funds in 2017. As a percentage of total market value, index-based mutual funds and ETFs also remain relatively small. As shown in Exhibit 1, domestic index mutual funds and ETFs comprised only 13% of total US stock market capitalization in 2017.

Exhibit 1. Investor Breakdown in the US Stock Market as a Percentage of Total US Stock Market Capitalization

In this context, it should also be noted that many investors use nominally passive vehicles, such as ETFs, to engage in traditionally active trading. For example, while both a value index ETF and growth index ETF may be classified as index investments, investors may actively trade between these funds based on short-term expectations, needs, circumstances, or for other reasons. In fact, several index ETFs regularly rank among the most actively traded securities in the market.

Beyond mutual funds, there are many other participants in financial markets, including individual security buyers and sellers, such as actively managed pension funds, hedge funds, and insurance companies, just to name a few. Security prices reflect the viewpoints of all these investors, not just the population of mutual funds.

As Professors Eugene Fama and Kenneth French point out in their blog post titled “Q&A: What if Everybody Indexed?”, the impact of an increase in indexed assets also depends to some extent on which market participants switch to indexing:

“If misinformed and uninformed active investors (who make prices less efficient) turn passive, the efficiency of prices improves. If some informed active investors turn passive, prices tend to become less efficient. But the effect can be small if there is sufficient competition among remaining informed active investors. The answer also depends on the costs of uncovering and evaluating relevant knowable information. If the costs are low, then not much active investing is needed to get efficient prices.”

What’s the volume?

Exhibit 2. Annual Global Equity Market Trading Volume, 2007–2018

In US dollars. Source: Dimensional, using data from Bloomberg LP. Includes primary and secondary exchange trading volume globally for equities. ETFs and funds are excluded.

Besides secondary market trading, there are also other paths to price discovery through which new information can get incorporated into market prices. For example, companies themselves can impact prices by issuing stock and repurchasing shares. In 2018 alone, there were 1,633 initial public offerings, 3,492 seasoned equity offerings, and 4,148 buybacks around the world.3 The derivatives markets also help incorporate new information into market prices as the prices of those financial instruments are linked to the prices of underlying equities and bonds. On an average day in 2018, market participants traded over 1.5 million options contracts and $225 billion worth of equity futures.

Hypothesis in practice

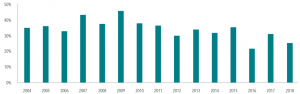

Exhibit 3. Active Manager Performance Has Not Improved

Percentage of Non-Index Equity Funds Outperforming for Three-Year Rolling Period, 2004–2018

Equity mutual fund outperformance percentages are shown for the three-year periods ending December 31 of each year, 2004–2018. Each sample includes equity funds available at the beginning of the three-year period. Outperformers are funds with return observations for every month of the three-year period whose cumulative net return over the period exceeded that of their respective Morningstar category index as of the start of the period. Past performance is no guarantee of future results.

Exhibit 4. Range of S&P 500 Index Constituent Returns

Upper chart includes 2008 total returns for constituent securities in the S&P 500 Index as of December 31, 2007. Lower chart includes 2017 total returns for constituent securities in the S&P 500 Index as of December 31, 2016. Excludes securities that delisted or were acquired during the year. Source: S&P data ©2019 S&P Dow Jones Indices LLC, a division of S&P Global. For illustrative purposes only. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Conclusion

Despite the increased popularity of index-based approaches, the data continue to support the idea that markets are working. Annual trading volume continues to be in line with prior years, indicating that market participant transactions are still driving price discovery. The majority of active mutual fund managers continue to underperform, suggesting that the rise of indexing has not made it easier to outguess market prices. Prices and returns of individual holdings within indices are not moving in lockstep with asset flows into index funds. Lastly, while naysayers will likely continue to point to indexing as a hidden danger in the market, it is important that investors keep in mind that index funds are still a small percentage of the diverse array of investor types. Investors can take comfort in knowing that markets are still functioning; willing buyers and sellers continue to meet and agree upon prices at which they desire to transact. It is also important to remember that while indexing has been a great financial innovation for many, it is only one solution in a large universe of different investment options.

Mutual Funds vs. ETF’s

Our partners at Charles Schwab produced this short video to help explain the difference between Exchange Traded Funds (ETF’s) and Mutual Funds. It’s common amongst investors to have little understanding of the difference between the two. There are times when it makes sense to choose one over the other. Timing, taxes and expenses are all factors.

Our partners at Charles Schwab produced this short video to help explain the difference between Exchange Traded Funds (ETF’s) and Mutual Funds. It’s common amongst investors to have little understanding of the difference between the two. There are times when it makes sense to choose one over the other. Timing, taxes and expenses are all factors.

Schwab now has over 2000 ETF’s and Mutual Funds that can be purchased with no commission or transaction cost. We help our clients navigate this broad universe of investment options, to build low cost portfolios designed to meet the client’s future goals. We can help you sift through the details when it comes time to invest your money.

Click on PLAY above to check out this SHORT, 3 minute clip, and call us if need help with your investment plan!

Getting to the Point of a Point

A quick online search for “Dow rallies 500 points” yields a cascade of news stories with similar titles, as does a similar search for “Dow drops 500 points.”

These types of headlines may make little sense to some investors, given that a “point” for the Dow and what it means to an individual’s portfolio may be unclear. The potential for misunderstanding also exists among even experienced market participants, given that index levels have risen over time and potential emotional anchors, such as a 500-point move, do not have the same impact on performance as they used to. With this in mind, we examine what a point move in the Dow means and the impact it may have on an investment portfolio.

Impact of index construction

The Dow Jones Industrial Average was first calculated in 1896 and currently consists of 30 large cap US stocks. The Dow is a price-weighted index, which is different than more common market capitalization-weighted indices.

An example may help put this difference in weighting methodology in perspective. Consider two companies that have a total market capitalization of $1,000. Company A has 1,000 shares outstanding that trade at $1 each, and Company B has 100 shares outstanding that trade at $10 each. In a market capitalization-weighted index, both companies would have the same weight since their total market caps are the same. However, in a price-weighted index, Company B would have a larger weight due to its higher stock price. This means that changes in Company B’s stock would be more impactful to a price-weighted index than they would be to a market cap-weighted index.

The relative advantages and disadvantages of these methodologies are interesting topics themselves, but the main purpose of discussing the differences in this context is to point out that design choices can have an impact on index performance. Investors should be aware of this impact when comparing their own portfolios’ performance to that of an index.

Headlines vs. reality

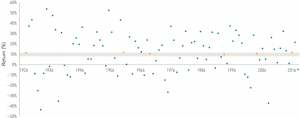

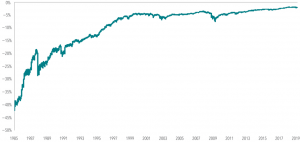

Movements in the Dow are often communicated in units known as points, which signify the change in the index level. Investors should be cautious when interpreting headlines that reference point movements, as a move of, say, 500 points in either direction is less meaningful now than in the past largely because the overall index level is higher today than it was many years ago.

Exhibit 1 plots what a decline of this magnitude has meant in percentage terms over time. A 500-point drop in January 1985, when the Dow was near 1,300, equated to a nearly 39% loss. A 500-point drop in December 2003, when the Dow was near 10,000, meant a much smaller 5% decline in value. And a 500-point drop in early December 2018, when the Dow hovered near 25,000, resulted in a 2% loss.

Exhibit 1. Hypothetical 500-Point Decline of the Dow Measured in Percentage Terms

How does the dow relate to your portfolio?

While the Dow and other indices are frequently interpreted as indicators of broader stock market performance, the stocks composing these indices may not be representative of an investor’s total portfolio.

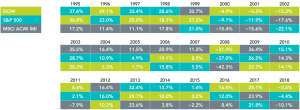

For context, the MSCI All Country World Investable Market Index (MSCI ACWI IMI) covers just over 8,700 large, mid, and small cap stocks in 23 developed and 24 emerging markets countries with a combined market cap of more than $50 trillion. The S&P 500 includes 505 large cap US stocks with approximately $23.8 trillion in combined market cap. The Dow is a collection of 30 large cap US stocks with a combined market cap of approximately $6.8 trillion.

Exhibit 2. Performance of MSCI ACWI IMI, S&P 500, and Dow by Calendar Year

Dow Jones and S&P 500 data © 2019 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. MSCI data © MSCI 2019, all rights reserved. MSCI ACWI IMI is the MSCI All Country World Investable Market Index (net dividends). Their performance does not reflect fees and expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results.

It is also important to note that some investors may be concerned about other asset classes besides stocks. Depending on investor needs, a diversified portfolio may include a mix of global stocks, bonds, commodities, and any number of other assets not represented in a stock index. A portfolio’s performance should always be evaluated within the context of an investor’s specific goals. Understanding how a personal portfolio compares to broadly published indices like the Dow can give investors context about how headlines apply to their own situation.

Conclusion

News headlines are often written to grab attention. A headline publicizing a 500-point move in the Dow may trigger an emotional response and, depending on the direction, sound either exciting or ominous enough to warrant reading the article. However, after digging further, we can see that the insights such headlines offer may be limited, especially if investors hold portfolios designed and managed daily to meet their individual goals, needs, and preferences in a broadly diversified and cost-effective manner.

Déjà Vu All Over Again

Investment fads are nothing new. When selecting strategies for their portfolios, investors are often tempted to seek out the latest and greatest investment opportunities. Over the years, these approaches have sought to capitalize on developments such as the perceived relative strength of particular geographic regions, technological changes in the economy, or the popularity of different natural resources. But long-term investors should be aware that letting short-term trends influence their investment approach may be counterproductive.

“There’s one robust new idea in finance that has

investment implications maybe every 10 or 15 years,

but there’s a marketing idea every week.” Nobel laureate Eugene Fama

What’s Hot Becomes What’s Not

Let’s look back at some investment fads over the decades:

1950’s – the “Nifty Fifty” (50 hot companies) were all the rage.

1960s – “go-go” stocks and funds piqued investor interest.

Late 20th century – emergence of a “new economy”

1990s – attention turned to the rising “Asian Tigers” of Hong Kong, Singapore, South Korea, and Taiwan.

2000’s – “BRIC” countries of Brazil, Russia, India, and China and their new place in global markets.

In the wake of the 2008 financial crisis – “Black Swan” funds, “tail-risk-hedging” strategies, and “liquid alternatives” abounded.

Recently – peer-to-peer lending, cryptocurrencies, and even cannabis cultivation

The Fund Graveyard

Unsurprisingly, however, numerous funds across the investment landscape were launched over the years only to subsequently close and fade from investor memory. While economic, demographic, technological, and environmental trends shape the world we live in, public markets aggregate a vast amount of dispersed information and drive it into security prices. Any individual trying to outguess the market by constantly trading in and out of what’s hot is competing against the extraordinary collective wisdom of millions of buyers and sellers around the world.

With the benefit of hindsight, it is easy to point out the fortune one could have amassed by making the right call on a specific industry, region, or individual security over a specific period. While these anecdotes can be entertaining, there is a wealth of compelling evidence that highlights the futility of attempting to identify mispricing in advance and profit from it.

It is important to remember that many investing fads, and indeed, most mutual funds, do not stand the test of time. A large proportion of funds fail to survive over the longer term. Of the 1,622 fixed income mutual funds in existence at the beginning of 2004, only 55% still existed at the end of 2018. Similarly, among equity mutual funds, only 51% of the 2,786 funds available to US-based investors at the beginning of 2004 endured.

What Am I Really Getting?

When confronted with choices about whether to add additional types of assets or strategies to a portfolio, it may be helpful to ask the following questions:

1. What is this strategy claiming to provide that is not already in my portfolio?

2. If it is not in my portfolio, can I reasonably expect that including it or focusing on it will increase expected returns, reduce expected volatility, or help me achieve my investment goal?

3. Am I comfortable with the range of potential outcomes?

If investors are left with doubts after asking any of these questions, it may be wise to use caution before proceeding. In addition, there is no shortage of things investors can do to help contribute to a better investment experience. Working closely with a financial advisor can help individual investors create a plan that fits their needs and risk tolerance. Pursuing a globally diversified approach; managing expenses, turnover, and taxes; and staying disciplined through market volatility can help improve investors’ chances of achieving their long-term financial goals.

Conclusion

Fashionable investment approaches will come and go, but investors should remember that a long-term, disciplined investment approach based on robust research and implementation may be the most reliable path to success in the global capital markets.

Self Employed? Set up a SEP and SAVE on Taxes before April!

Self-employed workers have an option for significant retirement savings that is UNDER-UTILIZED, yet so extremely simple. Experts estimate that Americans will need 70 to 90 percent of their preretirement income to maintain their current standard of living when they stop working. It’s crucial for the Self-employed to understand the opportunities in a Simplified Employee Pension (SEP) Plan.

Self-employed workers have an option for significant retirement savings that is UNDER-UTILIZED, yet so extremely simple. Experts estimate that Americans will need 70 to 90 percent of their preretirement income to maintain their current standard of living when they stop working. It’s crucial for the Self-employed to understand the opportunities in a Simplified Employee Pension (SEP) Plan.

A Simplified Employee Pension Plan (SEP IRA) is the easiest small business retirement plan to administer and maintain, and helps individuals and business owners get access to a significant tax deferred benefit when saving for retirement. A self-employed worker can defer up to 25% of their taxable income to a maximum of $56,000 per year. In comparison, a traditional IRA has a maximum of $6,000 annually.

If you’re self-employed, you work 24/7 and you save annually for a hefty tax bill in April. Neglecting to maximize retirement savings potential can be devastating now and in the future. The immediate impact of deferring a large amount of income to a SEP is a significant reduction in your tax liability. Long-term, you will be able to design your retirement experience without worry of outliving your money.

It’s not too late for 2018! You can open a SEP and fund it for 2018 up until the tax deadline!

Before making any long-term decisions about your retirement strategy, you should understand the ins and outs of a SEP IRA.

A SEP IRA…

- Requires very little paperwork

- Allows flexible contributions

- Allows investments to grow tax deferred

- Allows business owners to contribute up to the lesser of 25% of participants’ pay, or $56,000

- If you have an employee, you must fund your employees SEP at the same rate as your own.

If you’re interested saving on your 2018 tax bill, contact us about opening a SEP IRA today before the TAX DEADLINE. Email Kevin at [email protected] and request a free Business Owner’s Guide for Retirement and an introductory financial analysis.

2018 Annual Market Review

After logging strong returns in 2017, global equity markets delivered negative returns in US dollar terms in 2018. Common news stories in 2018 included reports on global economic growth, corporate earnings, record low unemployment in the US, the implementation of Brexit, US trade wars with China and other countries, and a flattening US Treasury yield curve. Global equity markets delivered positive returns through September, followed by a decline in the fourth quarter, resulting in a –4.4% return for the S&P 500 and –9.4% for the MSCI All Country World Index for the year.

The fourth quarter equity market decline has many investors wondering how equities may perform in the near term. Equity market declines of 10% have occurred numerous times in the past. The S&P 500 returned –13.5% in the fourth quarter while the MSCI All Country World Index returned –12.8%. After declines of 10% or more, equity returns over the subsequent 12 months have been positive 71% of the time in US markets and 72% of the time in other developed markets.

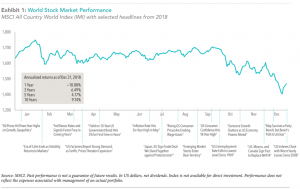

Exhibit 1 highlights some of the year’s prominent headlines in the context of global stock market performance as measured by the MSCI All Country World Index (IMI). These headlines are not offered to explain market returns. Instead, they serve as a reminder that investors should view daily events from a long-term perspective and avoid making investment decisions based solely on the news.

Market Volatility

Exhibit 2 shows the performance of markets subsequent to declines of 10%, 20%, and 30%. For each decline threshold, returns are shown for US large cap, non-US developed markets large cap, and emerging markets large cap stocks in the following 12-month period. While declines in equity markets may cause investor concern, the data provides evidence that markets generally have positive returns after a decline.

The increased market volatility in the fourth quarter of 2018 underscores the importance of following an investment approach based on diversification and discipline rather than prediction and timing. For investors to successfully predict markets, they must forecast future events more accurately than all other market participants and predict how other market participants will react to their forecasted events.

There is little evidence suggesting that either of these objectives can be accomplished on a consistent basis. Instead of attempting to outguess market prices, investors should take comfort that market prices quickly incorporate relevant information and that information will be reflected in expected returns.

While we cannot control markets, we can control how we invest. As Dimensional’s Co-CEO Dave Butler likes to say, “Control what you can control.”

WORLD ECONOMY

In 2018, the global economy continued to grow, with 44 of the 45 countries tracked by the Organization for Economic Cooperation and Development (OECD) on pace to expand. Argentina was the only country expected to contract. While market participants may consider the economic outlook of a region, it is just one of many inputs that determine realized market performance.

2018 MARKET PERSPECTIVE

Equity Market Highlights

Global equity markets, as measured by the MSCI All Country World Index, ended the year down –9.4%, with significant dispersion by country.

US equities generally outperformed other developed markets for the year, although they lagged other developed and emerging markets in the fourth quarter. The S&P 500 Index recorded a –4.4% total return for the year and –13.5% return in the fourth quarter.

Returns among other developed equity markets were negative. The MSCI World ex USA Index, which reflects non-US developed markets, was down –14.1% for the year and –12.8% for the fourth quarter, and the MSCI Emerging Markets Index fell –14.6% for the year and

–7.5% for the fourth quarter. US small cap stocks, as measured by the Russell 2000 Index, returned –11.0% for the year.

Impact of Global Diversification

While markets around the world generally had negative returns in the fourth quarter, the dispersion in their returns highlights the importance of global diversification during market declines. The MSCI All Country World ex USA Index (IMI) outpaced the S&P 500 for the quarter (–11.9% vs. –13.5%). Given the strong returns of US markets through September, however, the US equity market was one of the stronger performing markets for the year, ranking seventh out of the 47 countries in the MSCI All Country World Index (IMI).

The S&P 500 Index’s –4.4% return marked the end of nine consecutive positive annual returns. Despite the negative return this year, the S&P 500 has still produced a 13.1% annualized return for the 10 years ending December 31, 2018.

When considering individual countries, 46 out of 47 countries were down for the year. Using the MSCI All Country World Index (IMI) as a proxy, no countries posted positive returns among developed markets, and only Qatar managed a positive return among emerging markets. As is typically the case, country-level returns varied significantly. In developed markets, returns ranged from –24.1% in Belgium to 0.0% in New Zealand. In emerging markets, returns ranged from –41.3% in Turkey to 27.1% in Qatar—a spread of almost 70%. Large dispersion among country returns is common, with the average spread in emerging markets over the past 20 years of 90%. Without a reliable way to predict which country will deliver the highest returns, this large dispersion in returns between the best and worst performing countries again emphasizes the importance of maintaining a diversified approach when investing globally.

To emphasize this point, Israel went from being the worst performer in developed markets in 2017 (10.4%) to the second-best performer in 2018, returning –3.6%. Likewise, Qatar went from being the second worst performing emerging market country (–12.5%) in 2017 to being the best performer in 2018.

When considering investing outside the US, investors should remember that non-US stocks help provide valuable diversification benefits, and that recent performance is not a reliable indicator of future returns. It is worth noting that if we look at the past 20 years going back to 1999, US equity markets have only outperformed in 10 of those years—the same expected by chance. We can examine the potential opportunity cost associated with failing to diversify globally by reflecting on the period in global markets from 2000-2009, commonly known as the “lost decade” among US investors. While the S&P 500 recorded its worst ever 10-year cumulative total return of –9.1%, the MSCI World ex USA Index returned 17.5%, and the MSCI Emerging Markets Index returned 154.3%. In periods such as this, investors were rewarded for holding a globally diversified portfolio.

Currencies

Currency movements detracted from US dollar returns in 2018 for non-US dollar assets. The strengthening of the US dollar vs. weakening of non-US currencies had a negative impact on returns for US dollar investors with holdings in unhedged non-US dollar assets, and detracted 3.5% from the returns as measured by the difference in returns between the MSCI All Country World ex USA IMI Index in local returns vs. USD. The US dollar strengthened against most currencies, including the euro, the British pound, and the Canadian dollar, and weakened against the Japanese yen.

As with individual country returns, there is no reliable way to predict currency movements. Investors should be cautious about trying to time currencies based on the recent strong or weak performance of the US dollar or any other currency.

Broad Market Index Performance

In 2018, the MSCI Emerging Markets Value Index (IMI) outperformed its growth counterpart (–11.5% vs.

–18.4%). In developed markets, however, this was not the case. The Russell 3000 Value Index underperformed the Russell 3000 Growth Index (–8.6% vs. –2.1%) and the MSCI World ex USA Value Index (IMI) underperformed its growth index counterpart (-15.6% vs. –13.8%). Small cap stocks generally underperformed large cap stocks globally. For example, the Russell 2000 Index returned –11.0% relative to –4.8% for the Russell 1000 Index. Similarly, the MSCI World ex USA Index outperformed its small cap counterpart (–14.1% vs. –18.1%), and the MSCI Emerging Markets Index outperformed its small cap counterpart (–14.6% vs. –18.6%).

The mix of relative performance of value vs. growth stocks within and across regions this year serves as a reminder of the importance of integrating premiums when designing and managing portfolios. Within US equity markets, when at least one of the size, value, and profitability premiums has been negative in a given year, at least one of the other factors was positive 81% of the time. Positive premiums can contribute to relative returns during time periods when other premiums are negative.

US Market

In the US, small cap stocks underperformed large cap stocks, and value stocks underperformed growth stocks using Russell indices. The Russell 2000 Index declined –11.0% for the year vs. –4.8% for the Russell 1000. The Russell 3000 Value Index returned -8.6% in 2018 vs. –2.1% for the Russell 3000 Growth Index. The variation in returns between these indices is within historical norms. Since 1979, there has been an annual return difference of 6% or greater 60% of the time.

Developed ex US Markets

In developed ex US markets, small cap stocks underperformed large cap stocks and value stocks underperformed growth stocks. Despite underperformance in 2018, over both five- and 10-year periods, small cap stocks, as measured by the MSCI World ex USA Small Cap Index, have outperformed large caps, as measured by the MSCI World ex USA Index. Growth stocks, as measured by MSCI World ex USA Growth Index (IMI), returned –13.8%, outperforming value stocks, which returned –15.6% in 2018, as measured using the MSCI World ex USA Value Index (IMI).

Emerging Markets

In emerging markets, small cap stocks, as measured by the MSCI Emerging Markets Small Cap Index, underperformed large cap stocks, as measured by the MSCI Emerging Markets Index. However, over the past 10 years, small caps returned an annualized 9.9%, outperforming large caps, which returned 8.0%.

Value stocks returned –11.5% as measured by the MSCI Emerging Markets Value Index (IMI), outperforming growth stocks, which returned –18.4% using the MSCI Emerging Markets Growth Index (IMI). This was the sixth largest outperformance of value over growth in emerging markets since 1999.

The complementary behavior of size (small vs. large) and relative price (value vs. growth) in emerging markets in 2018 is a good example of the benefits of diversification. While small cap stocks underperformed, diversified portfolios were buoyed by outperformance among value stocks. This integration can increase the reliability of outperformance and mitigate the impact of an individual asset group’s underperformance.

Despite recent years’ headwinds, the size, value, and profitability premiums remain persistent over the long term and around the globe. It is well documented that stocks with higher expected return potential, such as small cap and value stocks, do not realize outperformance every year. Maintaining discipline to these parts of the market is the key to effectively pursuing the long-term returns associated with size, value, and profitability.

Fixed Income

Over the full year, the return on the US fixed income market was relatively flat; the Bloomberg Barclays US Aggregate Bond Index returned 0.0%. Non-US fixed income markets posted positive returns in 2018, contributing to the return of the Bloomberg Barclays Global Aggregate Bond Index (hedged to USD) at 1.8%.

Yield curves were upwardly sloped in many developed markets for the year, indicating positive expected term premiums. Realized term premiums were negative in the US as long-term maturities underperformed their shorter-term counterparts and positive in developed markets outside the US. For example, the FTSE Non-USD World Government Bond Index 10+ (hedged to USD) returned 4.4% for the year vs. 3.0% for the 1-10 Index.

Credit spreads, which are the difference between yields on lower quality and higher quality fixed income securities, widened during the year, as measured by the Bloomberg Barclays Global Aggregate Corporate Option Adjusted Spread. Realized credit premiums were negative both globally and in the US, as lower-quality investment-grade corporates underperformed their higher-quality investment-grade counterparts. Treasuries were the best performing sector globally, returning 2.8%, while corporate bonds returned –1.0%, as reflected in the Bloomberg Barclays Global Aggregate Bond Index (hedged to USD).

In the US, the yield curve flattened as interest rates increased more on the short end of the yield curve relative to the long end. The yield on the 3-month US Treasury bill increased 1.06% to end the year at 2.45%. The yield on the 2-year US Treasury note increased 0.59% to 2.48%. In other major markets, interest rates decreased in Germany and Japan, while they increased in the United Kingdom. Yields on Japanese and German government bonds with maturities as long as 10 years finished the year in negative territory. Conclusion 2018 included numerous examples of the difficulty of predicting the performance of markets, the importance of diversification, and the need to maintain discipline if investors want to effectively pursue the long-term returns the capital markets offer. The following quote by John “Mac” McQuown, a Dimensional Director,[6] provides useful perspective as investors head into 2019:“Modern finance is based primarily on scientific reasoning guided by theory, not subjectivity and speculation.”

Sources:

Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. S&P and Dow Jones data © 2019 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. MSCI data © MSCI 2019, all rights reserved. ICE BofAML index data © 2019 ICE Data Indices, LLC. Bloomberg Barclays data provided by Bloomberg. Indices are not available for direct investment; their performance does not reflect the expenses associated with the management of an actual portfolio.

Past performance is no guarantee of future results. This information is provided for educational purposes only and should not be considered investment advice or a solicitation to buy or sell securities. There is no guarantee an investing strategy will be successful. Diversification does not eliminate the risk of market loss.

Investing risks include loss of principal and fluctuating value. Small cap securities are subject to greater volatility than those in other asset categories. International investing involves special risks such as currency fluctuation and political instability. Investing in emerging markets may accentuate these risks. Sector-specific investments can also increase these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks, including changes in credit quality, liquidity, prepayments, and other factors. REIT risks include changes in real estate values and property taxes, interest rates, cash flow of underlying real estate assets, supply and demand, and the management skill and creditworthiness of the issuer.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Declines are defined as points in time, measured monthly, when the market’s return since the prior market maximum has declined by at least 10%. Declines after December 2017 are not included, but subsequent 12-month returns can include 2018 returns. Compound returns are computed for the 12 months after each decline observed and averaged across all declines for the cutoff. US markets (1926–2018) are represented by the S&P 500 and Developed ex US markets (1970–2018) are represented by the MSCI World ex USA Index.

OECD Real GDP Forecast, 2019. Accessed Jan. 4, 2019.

https://data.oecd.org/gdp/real-gdp-forecast.htm#indicator-chart Source: MSCI country investable market indices (net dividends) for each country listed. Does not include Greece, which MSCI classified as a developed market prior to November 2013. Additional countries excluded due to data availability or due to downgrades by MSCI from emerging to frontier market. MSCI data © MSCI 2019, all rights reserved. Past performance is no guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Measured from 1964 through 2017. In US dollars. Size premium: Dimensional International Small Cap Index minus the MSCI World ex USA Index (gross dividends). Relative price premium: Fama/French International Value Index minus the Fama/French International Growth Index. Profitability premium computed by Dimensional using Bloomberg data: Dimensional International High Profitability Index minus the Dimensional International Low Profitability Index. Profitability is measured as operating income before depreciation and amortization minus interest expense, scaled by book. Dimensional indices use Bloomberg data. Fama/French indices provided by Ken French. MSCI data copyright MSCI 2019, all rights reserved. The information shown here is derived from such indices. Index descriptions available upon request. Eugene Fama and Ken French are members of the Board of Directors of the general partner of, and provide consulting services to, Dimensional Fund Advisors LP. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is no guarantee of future results.

Source: The US Department of the Treasury

Dimensional Director refers to the Board of Directors of the general partner of Dimensional Fund Advisors LP.

Quarterly Market Review – Q4 2018

Click on the link below for a detailed analysis of quarterly performance of the global equity and fixed income markets.

CLICK HERE TO READ THE 4th QUARTER 2018- QUARTERLY MARKET REVIEW

Contribute to a 529 before December 31st!

The projected costs for college can be very intimidating…but there are ways to prepare for it. Just knowing the possible sticker price gives you the power to prepare! Without preparation, your retirement plan could be significantly impacted. If you have a future student, YOU MUST START PLANNING NOW! THE DEADLINE TO CONTRIBUTE TO A 529 FOR A 2018 TAX CREDIT IS FAST APPROACHING!

The projected costs for college can be very intimidating…but there are ways to prepare for it. Just knowing the possible sticker price gives you the power to prepare! Without preparation, your retirement plan could be significantly impacted. If you have a future student, YOU MUST START PLANNING NOW! THE DEADLINE TO CONTRIBUTE TO A 529 FOR A 2018 TAX CREDIT IS FAST APPROACHING!

THE IMPORTANCE OF INVESTING NOW

To help reduce the expected costs of funding future college expenses, parents can invest in assets that are expected to grow their savings at a rate of return that outpaces inflation. By doing this, college expenses may ultimately be funded with fewer dollars saved. Because these higher rates of return come with the risk of capital loss, this approach should make use of a robust risk management framework. With a tax-deferred savings vehicle, such as a 529 plan, parents will not pay taxes on the growth of their savings, which can help lower the cost of funding future college expenses. While there are stipulations as to how the money is spent, many states will give you a tax credit for investing in a 529. Indiana, for instance, offers a 20% tax credit on your deposits up to $5,000. That is a potential for a $1000 credit on your state taxes…an immediate 20% return.

Take a look at these estimates, and the impact a 529 investment plan can have on the price tag:

Estimated Total Cost of College in 18 Years = $190,000

Est. Total Amount Paid For College if Family invests $5,000/Year from birth to Age 18 = $90,000 of Savings + $100,000 of Projected Investment Growth. That is a total of $90,000 Out Of Pocket.

VERSES…

Est. Total Amount Paid if Family saves nothing and finances the total amount = $190,000 Borrowed + $46,000 in Interest. That is a total of $236,000 out of pocket.

If your goal is to fund college for your child, a price tag difference of $146,000 (not including tax credits you can capture along the way) can derail your retirement plans. $146,000 invested over 10 years at 7% is nearly $300,000.

RISK MANAGEMENT AND DIVERSIFICATION

Just as with your retirement portfolio, it’s important to work with a trusted advisor when saving for college expenses. A professional who has a transparent, diversified approach based on sound investment principles, consistency, and trust can help investors identify an appropriate risk management strategy. When saving for college, risk management assets (e.g., bonds) can help reduce the uncertainty of the level of college expenses a portfolio can support by enrollment time. These types of investments can help one tune out short‑term noise and bring more clarity to the overall investment process. As kids get closer to college age, the right balance of assets is likely to shift from high expected return growth assets to risk management assets.

CONCLUSION

Higher education may come with a high and increasing price tag, so it makes sense to plan well in advance. There are many unknowns involved in education planning, and no “one-size-fits-all” approach can solve the problem. By having a disciplined approach toward saving and investing, however, parents can remove some of the uncertainty from the process. A trusted advisor can help parents craft a plan to address their family’s higher education goals. The deadline for a 529 tax credit is DECEMBER 31st. If you need help with this goal, contact our firm and we can guide you to the right plan.